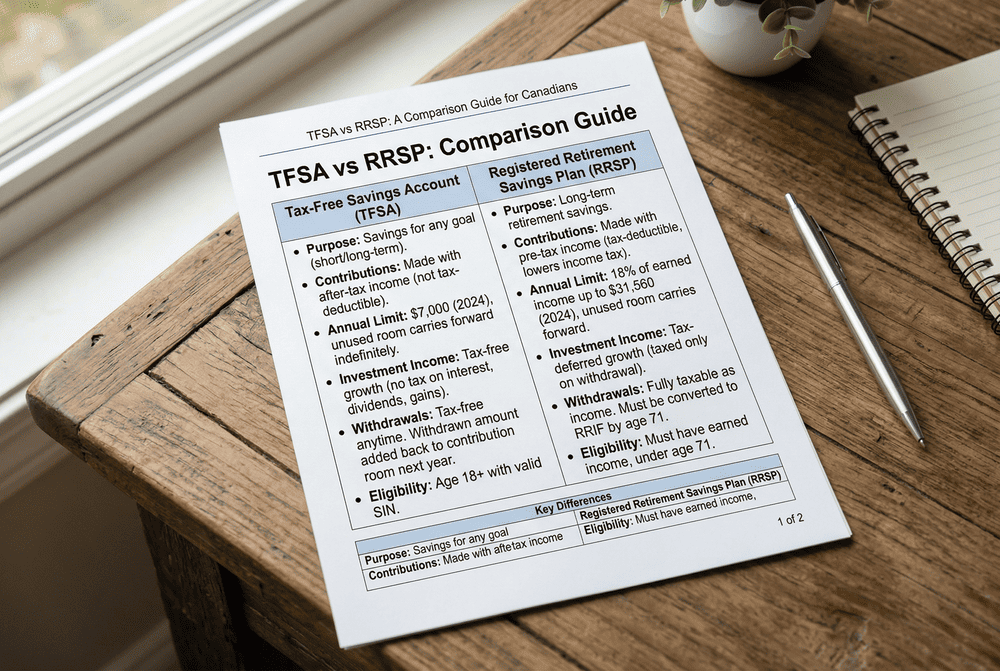

The main difference between an RRSP and a TFSA is when you get the tax break. With an RRSP, your contributions will reduce your taxable income today. You pay tax later, upon withdrawal.

With a TFSA, you contribute with after-tax dollars, but every dollar that grows inside it (and every dollar you take out) is completely tax-free.

That’s the simple answer. But the question of which one to prioritize, and in what order, is where most people in the 25–45 age range get tripped up. And it’s costing them.

Let’s break down the RRSP vs. TFSA decision in a way that actually makes sense for where you are right now.

Why the RRSP vs. TFSA Decision Isn’t About the Account

Here’s the mistake most people make: they treat the RRSP vs. TFSA question as a product comparison, like choosing between two smartphones. They Google which one earns more. They ask which one is “better.”

The real question isn’t about the account but your income trajectory.

The tax efficiency of each account depends almost entirely on the difference between your tax rate today and your expected tax rate at withdrawal.

Think of it this way:

- If you’re in a higher tax bracket now than you expect to be in retirement, the RRSP wins since you’re deferring tax from a high rate to a lower one.

- If you’re in a lower bracket now (or expect your income to grow significantly), the TFSA often wins, because you lock in your current lower rate, and future growth is untaxed.

- If you’re genuinely unsure, the answer is often to use both, strategically.

At Beyond Wealth, this is one of the first conversations we have with our clients. Not “which account,” but “what does your income look like now vs. later?”

How Contribution Limits Work for RRSP and TFSA Accounts

Understanding contribution room is critical — and it works very differently between the two accounts.

RRSP contribution room accumulates annually based on a percentage of your earned income from the prior year (to a maximum set by the CRA each year).

Unused room carries forward, which means if you didn’t contribute in previous years, that room is still available to you. Your total available room is visible on your Notice of Assessment from the CRA.

TFSA contribution room accrues every year for any Canadian resident aged 18 or older, regardless of income.

Unused room also carries forward and, importantly, any amount you withdraw from a TFSA is added back to your contribution room the following year. That’s a flexibility feature the RRSP doesn’t offer.

The key questions to ask before contribution season:

- Do you know your current RRSP contribution room? (Check your CRA My Account)

- Have you carried forward unused TFSA room from previous years?

- Are there life events — a job change, a bonus, parental leave — that affect your income this year?

You don’t have to answer them alone. Your advisor at Beyond Wealth can pull your full picture and help sequence contributions around your actual tax situation.

What Are the Tax Benefits of Using an RRSP Versus TFSA?

Both accounts offer tax advantages. They just deliver them at different points in time.

RRSP tax benefits: Contributions reduce your net income for the year you claim them. That can lower your tax bill immediately, trigger or increase government benefits calculated on net income (like the Canada Child Benefit) and build a tax-deferred savings pool for retirement.

The catch: every dollar you withdraw is taxed as income at your marginal rate at the time.

TFSA tax benefits: There’s no upfront deduction. You’re contributing money you’ve already paid tax on. But inside the account, growth is completely sheltered from tax. Dividends, capital gains, interest, none of them are taxable.

And withdrawals don’t count as income, which means they won’t affect income-tested benefits.

For many clients who are at the stage of professional growth, the smartest RRSP vs. TFSA strategy isn’t either/or. It’s a sequencing question: which one do you fill first, and why, given your specific income, tax bracket, and goals?

That’s what a life-stage financial plan is designed to answer.

Can You Transfer Your RRSP to a TFSA?

This is one of the most common RRSP vs. TFSA questions we hear.

And the answer is: not directly.

You cannot transfer funds from an RRSP to a TFSA without a taxable event. Withdrawing from an RRSP triggers income tax in the year of withdrawal. You could then contribute those (now after-tax) dollars to your TFSA, but only if you have available TFSA contribution room, and only after accounting for the tax hit.

In some circumstances, this can make sense, for example, in a year where your income is unusually low. But it’s a decision that still requires careful planning.

If you’re thinking about restructuring your accounts, speak with your advisor before making any changes. At Beyond Wealth, we map out the full tax impact before recommending any RRSP or TFSA shifts.

The Mid-30s Trap: When Doing Something Is Still Wrong

Here’s something worth naming directly: many people in their 30s are contributing to one or both accounts, but not in the right order, in the right amounts, or for the right reasons.

The most common patterns we see:

- Defaulting to RRSP every year without considering whether a TFSA would be more efficient given current income

- Maxing TFSA contributions without realizing they have years of unused RRSP room that could significantly reduce their current tax bill

- Treating the RRSP contribution deadline as a once-a-year event rather than a year-round strategy

- Not adjusting the strategy after a major life change — new job, promotion, marriage, or a child

None of these are catastrophic. But over 10 or 15 years, the compounding cost of the wrong sequencing adds up. The RRSP vs. TFSA decision is something worth revisiting every year with a clear-eyed look at your current situation.

Where to Invest in an RRSP or TFSA: The Question Behind the Question

People often search for the best RRSP and TFSA options at specific financial institutions, looking for the lowest fees or the highest rates. And while cost matters, it’s secondary to strategy.

What matters more:

- Are your contributions being invested, not just sitting in cash?

- Is your asset mix appropriate for your time horizon and risk profile?

- Are your RRSP and TFSA investments coordinated with each other and your overall financial picture?

At Beyond Wealth, we work across both accounts as part of an integrated plan, not as two separate buckets. That coordination is where the real value tends to live.

Frequently Asked Questions

What is the difference between a TFSA and an RRSP?

The core difference is timing. An RRSP reduces your taxable income now and taxes you on withdrawal. A TFSA uses after-tax money, but all growth and withdrawals are completely tax-free. The right choice depends on whether your tax rate is higher now or expected to be higher later.

How do contribution limits work for RRSP and TFSA accounts?

RRSP room is earned. It’s based on a percentage of your prior year’s earned income, up to an annual CRA maximum. TFSA room accrues each year automatically for eligible Canadians, regardless of income. Both types of unused room carry forward. TFSA room is also restored the year after a withdrawal, giving it more flexibility.

What are the tax benefits of using an RRSP versus a TFSA?

RRSP contributions lower your net income today, which can reduce your current tax bill and affect income-tested benefits. TFSA contributions don’t offer an upfront deduction, but all growth is tax-free and withdrawals don’t count as income. For many people, using both, in the right sequence, delivers the best tax outcome over time.

Where can I invest in an RRSP with low fees?

Low fees matter, but they’re only one part of the equation. What’s inside the account — the investment mix, the asset allocation, how it coordinates with your other accounts — tends to have a bigger impact on long-term outcomes than fees alone. A good advisor will help you optimize both. As a starting point, questions to ask any financial institution include: what’s the MER on the funds available? Are there account fees? What does the investment selection look like?

Not sure which account to prioritize this year?

The RRSP vs. TFSA decision looks different for everyone, and it changes as your income and life evolve. Book a review call with a Beyond Wealth advisor to get a clear picture of where you stand and what sequence makes sense for you.

This article is educational in nature and does not constitute financial, tax, or legal advice. For guidance specific to your situation, please speak with a qualified financial advisor.

© 2026 Beyond Wealth Management Canada. All rights reserved.